One of the most difficult parts of tracing freedpeople is finding information on them from before the 1870 federal census. Every piece of evidence from after the Civil War up to the 1870 census is valuable.

A complicating factor is that surname usage among freedmen was not necessarily stable during this period and for some time afterward. Liberty County freedpeople have been found to “change” surnames between the 1870 and 1880 census. Differing surnames for the same person mentioned in the Freedman’s Bank records also reveal possible differences between surnames used informally during slavery and surnames chosen afterward.

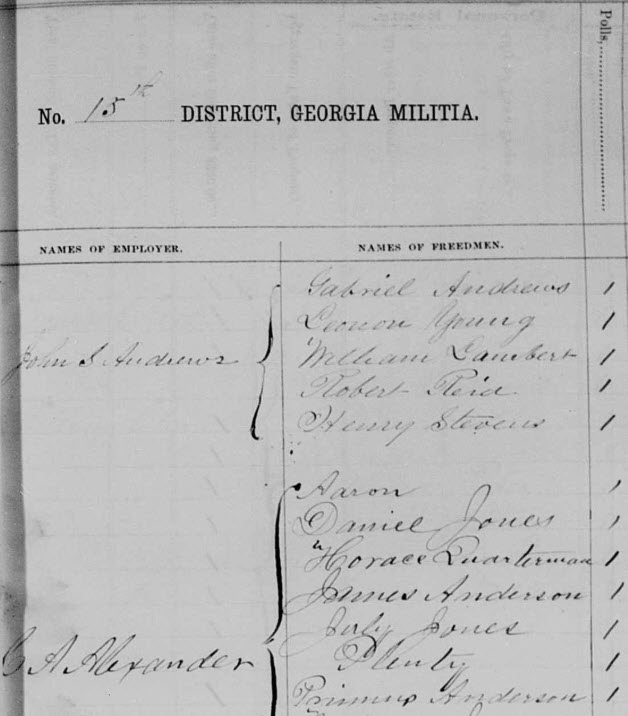

In Liberty County and elsewhere, tax records provide critical clues. After the dust settled from the Civil War, a structure had to be created to add newly freed people to the tax rolls, though most of them had little to nothing to tax and few resources to use to pay the taxes. The one tax that no one could escape was the $1 poll tax, assessed on all males between 21 and 60 years or age. How to deal with men who could not pay the tax? For anyone without property who was employed by someone else as a laborer, the employer was responsible for paying the tax, but could deduct it from the laborer’s wages.**

This resulted in a remarkable set of documents. For 1867-1869, the Liberty County tax digest listed all freedmen of poll-tax age AND grouped them by employer. It is likely that the information was received from the employer; some of the freedmen were listed without surnames. This could be because the freedman’s chosen surname was not known to the employer but also could be the employer’s lack of interest in the name or the task. For example, Roswell King’s employees were listed with surnames in 1867 and 1868 but without in 1869. The digest also listed any property owned by the freedmen.

I’ve transcribed the 1867-1869 freedmen/employer lists into a spreadsheet that contains 2132 names. It’s now on the website as a sortable list: https://theyhadnames.net/freedmen-employer-tax-digest-lists-1867-1869/. (The format on the website is functional for looking for particular names but if you’re doing anything more complicated, email jnscole@yahoo.com and I’ll send you a copy of the spreadsheet.)

Are the employers likely to be the last enslavers? Possibly. It must be remembered that many slaveowners left Liberty County during the war and may not have returned, or were not in a position after the war to employ people. But it’s at least a clue. A place to start researching would be to compare the lists across years to see if the freedman of interest stays with the same employer.

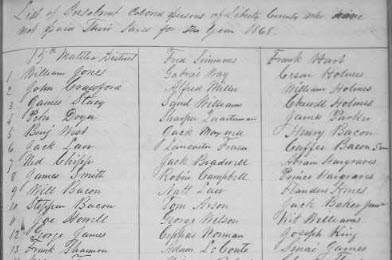

Another recently added list to use in conjunction with the tax digest list is an 1868 record of 464 freedmen who were said to have not paid their 1868 taxes. The Liberty County Grand Jury compiled lists each year of insolvent taxpayers. It is not clear how this correlates with the fact that employers were responsible for paying the poll tax, but 120+ freedmen were indicted after voting in the 1868 Presidential election after supposedly swearing they had paid their taxes. It does not appear that they were ever prosecuted, though.

The other hugely useful document from this time period is the 1867 voter registration documents. These consist of books for the reconstruction oaths that all men, white or black, had to take in order to be able to vote; an overall list of all the men who registered to vote; and most helpful, an overall list that identifies the men by race AND gives the number of years they’ve lived in the state, county, and precinct, which often correlates to age. Those documents are available on FamilySearch.org and Ancestry.com but I’m also in the process of transcribing them to put on the website as a sortable spreadsheet (hopefully to be finished in the next few weeks).

Other useful records on the website for researching this time period:

- Freedmen started filing homestead exemptions as early as 1868: https://theyhadnames.net/homestead-exemption-petitions-1868-1900/.

- Post-war labor contracts between freedmen and employers, mediated by the Freedmen’s Bureau: https://theyhadnames.net/freedmens-bureau-records/

- Marriages of freedpeople, 1866-1874: https://theyhadnames.net/liberty-county-african-american-marriages-1865-1874/

- Postbellum bonds for orphans and apprentices: https://theyhadnames.net/postbellum-orphan-bonds-and-apprentices/

- and of course, the Southern Claims Commission petitions: https://theyhadnames.net/freedmens-bureau-records/

**Thanks for David Paterson for this information! Acts of the General Assembly of the state of Georgia, passed in Milledgeville, at an annual session, in November and December, 1866 [volume 1], p. 164: “In addition to the ad valorem tax on real and personal property, as specified in the Code and assessed in the preceding section, the following specific taxes shall be levied and collected: a tax of one dollar upon each and every male inhabitant of this State on the first day of April, between the ages of twenty-one and sixty years. When this tax is due and unpaid by any person who has no property and is in the employment of another as a laborer, it shall be the duty of the Tax Collector to serve a written notice on the employer, specifying the amount of tax due by the employee, and shall authorize and bind him to pay said tax from any wages, effects or money in his hands, due to the laborer or employee, and execution shall issue, as in other cases for taxes due, against the employer for the amount.”